Maintaining management accounting in 1C. What is management accounting? Setting up management accounting from scratch in 1c

Management accounting is extremely important for the successful existence of an enterprise. Automation tools that have emerged over the past few decades have greatly simplified this matter. So, what is management accounting in 1C 8.3?

general information

The choice of the optimal way to solve problems is ambiguous and largely depends on the specifics of the work being carried out and the structural organization of the internal information system. Although there are plenty of coinciding moments. First of all, you need to pay attention to the configuration of the information system. And here we need to start from the very beginning - design. The stability and uninterrupted operation of the entire system largely depends on this. If you don’t set it up from the very beginning, it will cause a lot of inconvenience in the future.

What is management accounting?

In "1C" 8.3 there are quite a large number of possibilities. For some, this is payment planning, others use the system to form budgets, and others calculate profits received from the sale of goods. Therefore, when building the entire system, it is necessary to decide for what purpose it will be used. Moreover, here it is necessary to look for a middle ground - so that at the same time there is an understanding of the situation at the enterprise, and not to be overloaded with data that you are familiar with - the situation has already changed.

Management accounting is also possible in 1C: Accounting, but it must be remembered that it cannot exist independently. It is always based on data that is supplied and informs about the operational situation. Although reflecting transactions in real time is not always necessary. But what you should take care of is their financial assessment. Although the main requirement is that the data arrive on time. Here, a lot depends on the company’s activities, the specifics of the data requirements on the basis of which reports are generated and the periods for their provision. One information should be submitted daily, the second - quarterly, and the third - upon request.

What's the point?

When people talk about management accounting in 1C:Enterprise, they often clarify that it should be more detailed and accurate than accounting. Of course, this may well be the case. But not necessarily. After all, management accounting in 1C:UPP is a powerful tool, the main purpose of which is to provide accounting in the chart of accounts and when working with registers. Therefore, if the accounting department covers all requests, then at the beginning of the next period you can have all the necessary data. But it should be understood that there are many different factors that have a significant impact on the “correctness” of the information collected and its compliance with the goals of the management. Let's say we are working with a counterparty. The owner of the partner company has not changed during this time. But the sign, legal address and name - more than once. Therefore, there will be several counterparties in the accounting department. Although for management accounting it is desirable to display it as one company. Therefore, working on the basis of accounting data is more suitable for small companies.

When people talk about management accounting in 1C:Enterprise, they often clarify that it should be more detailed and accurate than accounting. Of course, this may well be the case. But not necessarily. After all, management accounting in 1C:UPP is a powerful tool, the main purpose of which is to provide accounting in the chart of accounts and when working with registers. Therefore, if the accounting department covers all requests, then at the beginning of the next period you can have all the necessary data. But it should be understood that there are many different factors that have a significant impact on the “correctness” of the information collected and its compliance with the goals of the management. Let's say we are working with a counterparty. The owner of the partner company has not changed during this time. But the sign, legal address and name - more than once. Therefore, there will be several counterparties in the accounting department. Although for management accounting it is desirable to display it as one company. Therefore, working on the basis of accounting data is more suitable for small companies.

What software should I use?

Of course, we already have 1C:Enterprise. But basic capabilities are often lacking. Therefore, add-ons and settings produced by various companies are often used. As an example, we can consider "1C BIT.FINANCE.Management Accounting". It is suitable for those who want to consolidate reporting, bring it into line with the requirements of international standards, provide multi-variant budget planning, and allow keeping records of all contracts. You can also work with "1C BIT.FINANCE.Management Accounting" from a mobile device, which allows you to flexibly and quickly respond to emerging needs. True, it is impossible to satisfy everyone with one development. And here we can additionally recommend using “1C:ERP Management Accounting”. This configuration is designed for employees of economic planning services, middle and senior managers.

Individual moments in perception

For many, when they talk about 1C - accounting, management accounting, the first is classified as white (fiscal), and the second - as real, clarifying the existing state of affairs. Yes, this can happen. But not necessarily. There are many companies that work honestly and do not hide anything. Therefore, the concept of accounting and management accounting can be applied to them. But what if some of the information should not be presented in the BU? There are options here too. Let's look at one of them:

For many, when they talk about 1C - accounting, management accounting, the first is classified as white (fiscal), and the second - as real, clarifying the existing state of affairs. Yes, this can happen. But not necessarily. There are many companies that work honestly and do not hide anything. Therefore, the concept of accounting and management accounting can be applied to them. But what if some of the information should not be presented in the BU? There are options here too. Let's look at one of them:

- Two organizations are created in the database. One can be given a real name, and the second can be called, for example, “Managerial”.

- All primary documentation is entered into the second database. If the document must be displayed in white accounting, then you can configure its automatic copying to the database with the real name of the organization.

- A similar approach can be used when solving the consolidation problem. For example, if a company includes several legal entities and you need to exclude transactions within the group.

To what extent these approaches can be applied, each manager of an individual enterprise must decide for himself.

About the relevance of the data

You can often hear that management accounting in 1C shows current data and that it is more efficient than accounting. Well, there is some truth in this, but not always. Let's consider this example. Shop accountants promptly reflect in accounting the closure of existing orders for the production of certain goods. Whereas it does not go to the BU or progresses with significant delays. But this is unlikely to be useful for a person who holds the position of financial director. Rather, it is aimed at production managers, salespeople and middle managers. Not all data needs to be displayed in the OU. But on the other hand, the accounting department records employee advance reports in accounting. And there is one technical feature here.

You can often hear that management accounting in 1C shows current data and that it is more efficient than accounting. Well, there is some truth in this, but not always. Let's consider this example. Shop accountants promptly reflect in accounting the closure of existing orders for the production of certain goods. Whereas it does not go to the BU or progresses with significant delays. But this is unlikely to be useful for a person who holds the position of financial director. Rather, it is aimed at production managers, salespeople and middle managers. Not all data needs to be displayed in the OU. But on the other hand, the accounting department records employee advance reports in accounting. And there is one technical feature here.

Employees may periodically forget to bring the necessary documents (air tickets, travel cards). And therefore, advance reports will not be issued promptly, but retroactively. This state of affairs is quite common. But! If services are provided by a counterparty company, then they must provide a certificate of completion of work. And if there is a delay, then accounts receivable will be formed in accounting. Whereas, according to the CU, it should not exist. In addition, management accounting in 1C assumes earlier closing of the period (usually no later than the tenth day).

About planning

Another important point. The accounting report is more focused on the past and records accomplished facts of economic activity. Whereas management accounting is created to enable planning for the future. But there are some nuances here. So, first of all, it is necessary to ensure automation of necessary tasks (for example, budgeting). But to avoid unpleasant moments, it is necessary to take care of plan-fact analysis and updating.

For what?

So, why can management accounting be implemented in 1C: Accounting 8.3? It is necessary in cases where you need to know about cash flow, income, expenses and management balance sheet. Separate and close attention is necessary for the goals that are set for the leader. After all, you can cram a lot of data into management accounting. But will they be useful? We should also not forget about automation of information processing. After all, if managers process and sort a large number of reports, many of which are simply not needed, then their work efficiency will decrease. And even to make successful decisions they will need many times more time than with proper organization of work.

So, why can management accounting be implemented in 1C: Accounting 8.3? It is necessary in cases where you need to know about cash flow, income, expenses and management balance sheet. Separate and close attention is necessary for the goals that are set for the leader. After all, you can cram a lot of data into management accounting. But will they be useful? We should also not forget about automation of information processing. After all, if managers process and sort a large number of reports, many of which are simply not needed, then their work efficiency will decrease. And even to make successful decisions they will need many times more time than with proper organization of work.

Basic tasks and difficulties in solving them

So, we reviewed the programs, management accounting "1C" and the differences between management and accounting. Now let's talk about practice. First of all, it is necessary to note the fact that reports created within the framework of management and accounting may be the same in form, but strikingly different in their content. This is most relevant in matters of detail (analytics) and financial assessment of indicators. In the future, the emphasis will be on management accounting. When generating reports on income and expenses, they contain a breakdown of cost centers. This is necessary to determine who brings more income and/or expenses, both in absolute and relative terms. Cash flow reports are also generated according to a similar principle. At the same time, the link goes not only to the items, but also to the places where expenses occur.

So, we reviewed the programs, management accounting "1C" and the differences between management and accounting. Now let's talk about practice. First of all, it is necessary to note the fact that reports created within the framework of management and accounting may be the same in form, but strikingly different in their content. This is most relevant in matters of detail (analytics) and financial assessment of indicators. In the future, the emphasis will be on management accounting. When generating reports on income and expenses, they contain a breakdown of cost centers. This is necessary to determine who brings more income and/or expenses, both in absolute and relative terms. Cash flow reports are also generated according to a similar principle. At the same time, the link goes not only to the items, but also to the places where expenses occur.

The most difficult point is the management balance. For the previous examples, it was enough to take into account only turnover indicators. Whereas for managerial balance it is necessary to provide attention to the remainder. Also, when compiling it, it is often necessary to indicate the direction of activity if the company is multidisciplinary. To simplify this task, product groups can be created with the subsequent distribution of assortment between them.

First example

Let's say the Construction company has an information technology department that maintains computerized equipment and software. The consumers of their services are various construction teams, which include complex construction equipment. At the same time, the IT department is formed as an independent organization A and is on a separate balance sheet. At the end of each month, a certificate of completion of work is transferred from her to another organization B, which is directly involved in construction. In regulatory accounting, income A and expenses B arise. But they have the same owner! Therefore, all this movement should not happen, because everything happens within the framework of one company. But for management accounting, it is still necessary to take into account the costs incurred by the information technology department. After all, servicing programs and equipment is not free, and besides, you need to pay salaries to employees.

Second example

Let's say that we have a company where goods go through a certain supply chain through several departments. Initially they are in a wholesale warehouse, then in a regional distribution center and end up in a retail sales division. Let us assume that the following conditions are met:

Let's say that we have a company where goods go through a certain supply chain through several departments. Initially they are in a wholesale warehouse, then in a regional distribution center and end up in a retail sales division. Let us assume that the following conditions are met:

- All listed divisions are part of one organization with a single owner.

- The management accounting policy provides that income is calculated exclusively on the product that is sold to the end consumer.

When products are sold on the market, the participation of all departments must be taken into account. For this purpose, the so-called through profitability is calculated. That is, in management accounting it is necessary to provide for the possibility of registering the movement of goods through warehouse premises. But it is also necessary to take into account such a point, which is often missed, as transfer prices, which include the cost of moving products between different points. And taking all this into account, the final indicators should be formed.

Management accounting is a system for collecting, registering, summarizing and providing objective information on the activities of an organization necessary for decision-making by the management level of the organization (managers). Thanks to the organization and implementation of a management accounting system, it becomes possible to analyze the financial and economic state of the enterprise, allocate resources, optimize costs, and improve financial performance indicators.

Objectives of management accounting, methods and means of their implementation

The introduction of management accounting allows you to effectively and efficiently solve a set of problems:

- Carry out planning of economic activities through budgeting;

- Control and optimize costs by promptly obtaining information;

- Analyze the deviation of actual indicators from planned ones based on management reports.

Ways to implement management accounting tasks:

- Management (internal) and financial (external) reporting;

- Operational accounting;

- Budgeting.

The means of implementation are:

- Budget of income and expenses;

- Cash flow budget;

- Forecast (planned) balance.

In accordance with all types of budgets used at enterprises in Moscow or in small towns in remote regions of Russia, automation of enterprise management accounting allows for monitoring the implementation of plans, analyzing the deviation of actual indicators from budget ones, making adjustments, and making management decisions. At the end of the planning period, the following are compiled:

- Cash flow statement;

- Gains and losses report;

- Balance.

Basic principles of policy for organizing a management accounting system

The organization of management accounting is based on certain principles of the company’s management policy. These include:

- Frequency corresponding to production cycles.

- Continuity of information and its repeated use.

- Formation of reporting indicators acceptable for all levels of management.

- Application of budgeting.

- Evaluation of the performance of individual structural divisions (CFD).

- Reliability, completeness, efficiency of information, possibility of analysis.

- Use of common units of measurement.

Requirements for the management accounting system at the enterprise

Automation of management accounting of an enterprise must meet certain requirements:

- Completeness and objectivity of displaying all facts of economic activity.

- Timely recording and provision of data.

- Relevance of indicators.

- Integrity of the management accounting system.

- Clear for all users.

- Regularity.

Objects of management accounting

Cost accounting is one of the most important tasks of enterprise management accounting. The objectivity and efficiency of information received by managers at all levels, especially in terms of costs, affects the effectiveness of the decisions they make. Therefore, the process of timely recording of resource use indicators is very relevant in the current activities of enterprises in Moscow and other regions of the Russian Federation. Its effective implementation is possible through the use of management accounting software. The set of management accounting objects can be combined into groups:

- Production resources;

- Economic processes;

- Income and expenses;

- Structural units (with localization of income and costs by place of origin (CF)).

Budgeting in management accounting

The budgeting process allows you to systematize enterprise management, determine goals and ways to achieve them, thanks to the planning and specification of indicators for all areas of activity and structural divisions. The organization of budgeting is carried out by centers of financial responsibility, by distributing functions, powers and responsibilities, determining the area of responsibility, and forming certain types of plans with maximum detail. This approach allows:

- achieve planned goals;

- optimize costs;

- rational use of resources;

- optimally distribute funds;

- improve the performance of business activities in general.

Enterprise Forecasting

The formation of a budget model depends on the specifics and type of activity of the enterprise. But the same principles are still used in its creation.

1. Budgetary integration. To ensure planning efficiency, a significant number of types of budgets can be created: operational and financial. They can be formed for each Central Federal District individually. But they are all interconnected and combined into a common budget system. The master plan is the company's consolidated budget.

2. The principle of consistency. All budgets are drawn up in accordance with certain regulations and are interconnected with each other. The primary ones are operating budgets, the indicators of which are summarized in the overall Budget of Income and Expenses, sometimes called the Profit and Loss Budget. On its basis, financial types of budgets are compiled: cash flow budget, forecast balance, capital budget.

3. The budgeting system is implemented on the basis of regulations (certain norms and standards).

4. End-to-end budgeting. The consolidated budget combines all types of enterprise plans, all of them are interconnected with each other.

5. Methodological comparability. When drawing up all types of budgets, uniform methodologies and approaches are used. This is necessary in order to carry out qualitative analysis and control over the implementation of plans based on comparable indicators.

Organization of management accounting

All types of reporting that accompany management accounting are sources of information for analysis. In synthesis with the reports used in budgeting, they are the basis for:

- decision making,

- assessing the financial condition of the company, its solvency and liquidity,

- forecasting development dynamics in the future,

- investment attractiveness,

- identifying bottlenecks and developing measures to eliminate them,

- adjustments to plans,

- monitoring the execution of plans,

- cost optimization,

- rational distribution of income,

- preventing cash gaps (current shortage of funds),

- system resource management,

- optimizing the quantity of inventory,

- determining the sufficiency of own funds for the implementation of investment projects,

- the need to attract borrowed funds for the successful implementation of new technologies and the purchase of fixed assets;

- identifying promising areas of development,

- analysis of deviations of actual indicators from planned ones in order to monitor the execution of budgets and adjust them to achieve set goals;

- implementation of measures aimed at improving financial performance results in general.

The main goal of management accounting is to find reserves to improve the efficiency of the enterprise. All information obtained through automation of management accounting should be in demand by managers at all levels, be of economic interest to them and be the basis for making rational decisions that contribute to the further positive development of the company.

Types of management reporting

All types of management reporting must eliminate uncertainty and provide an objective picture, which is necessary for the performance of management functions. Therefore, for example, automation of management accounting is a system of related indicators that have a full set of characteristics necessary to justify decisions based on objective data.

All types of management reporting have standard forms (in accordance with the approved Accounting Policies), but they can be detailed depending on the company’s needs for data decoding. For example, to determine categories of potential buyers or priority groups of goods, a special report can be used that involves generalizing the range of goods and target buyers according to a number of characteristics.

Formation of management accounting

The formation of management accounting can be grouped into three main blocks:

- Reporting on the financial position of the company and its changes, results of operations.

- Reporting on key performance indicators.

- Reporting on budget execution.

Most often, at enterprises where projects are implemented for the purpose of administrative accounting, the following reporting forms are used:

- Cash flow statement

- Sales report

- Production report

- Procurement report

- Raw Materials Inventory Report

- Finished Products Report

- Accounts receivable report

- Accounts payable report.

For an unambiguous interpretation of objects, various classifiers can be used. Their types and quantity are determined based on the needs of the company and are enshrined in the provisions of the management policy, which is formed by the administrative accounting department.

At enterprises in Moscow and other cities in the Russian Federation, the following types of classifiers are most often used:

- Types of products

- Types of work

- Types of services

- Types of income

- Cost centers

- Financial Responsibility Centers

- Types of costs

- Types of assets

- Types of equity capital

- Types of obligations

- Directions of investment

- Projects

- Main and auxiliary business processes

- Personnel categories

- Categories of counterparties.

The chart of accounts for management accounting “WA: Financier” can correspond to standard accounting (financial) accounts. It is a tool for systematically displaying information and grouping it according to general characteristics. The chart of accounts can be formed in accordance with the objectives of the company; it allows you to systematically accumulate all information about the economic activities of the enterprise.

Common features and differences between management and financial reporting

All enterprises in Moscow and other cities of Russia must keep financial records, since they are regulated by the legislation of the Russian Federation. Its purpose is to provide information for external users, including government agencies (for example, the tax inspectorate). The purpose of introducing management accounting tools is to provide complete and objective information for internal users, which can facilitate the adoption of effective management decisions. Internal information may be the subject of a trade secret and its dissemination outside the company may be accompanied by sanctions against violators. Financial statements are the basis for analyzing the financial viability of a company, used by investors, creditors or other parties interested in investing capital. The formation of management accounting is primarily the basis for effective management, since it displays objective information about the current financial condition of the enterprise. With its help, operational decisions can be made in order to respond in a timely manner to changes in the external situation or adjust paths that contribute to the achievement of strategic goals.

Financial reporting forms are standardized, therefore understandable to external users and comparable in terms of indicators. Forms of internal management reporting can be varied and are approved in accordance with company regulations. But in turn, they must also be unified in order for performance indicators to be comparable across the functioning of individual structural units.

Management and financial systems are interconnected and have commonality:

- Unified objects;

- General approach to defining goals and monitoring their achievement;

- Similar principles if an identical chart of accounts is used;

- One-time input of primary data;

- The information base is used for analysis and management decision-making;

- Application of similar techniques.

Many business transactions in the financial and management systems are displayed identically, others still require a specific approach, depending on the company policy applied to the management system. These two types of accounting also have significant differences; they relate to the following aspects:

- Periodicity. In management, reporting periods are regulated by internal Regulations, in financial – by state legislation.

- Nature of indicators. In financial - all indicators are measured in value terms, in management - the range of units of measurement is wider; in addition to cost criteria, natural values and quality indicators can be used.

- Level of detail. Management reporting presents analytical information in more detail.

- Method of grouping data. The two systems may use different principles for grouping information.

- The degree of accuracy of the information. In management, tolerances are possible, that is, certain errors, which are unacceptable in finance.

The main stages of setting up and implementing automation of management accounting

The main stages of setting up and implementing automation of management accounting include:

- Development and approval of technical specifications

- Development of a company strategy with identification of goals and priority areas

- Analysis and diagnostics of the existing organizational structure, system of financial and economic relations, organization of production, planning and accounting systems.

- Creation of an information base for the implementation of a management system.

- Development of the company's financial structure and identification of financial responsibility centers.

- Development of a cost management system, classification of costs.

- Formation of a management reporting system.

- Construction of a budgeting system.

- Introduction of administrative accounting.

- Process automation.

At each stage of setting tasks and implementing automation of management accounting, appropriate regulations are developed that define norms and rules. They are displayed in specific Regulations, which are documents reflecting company policy.

Methodological approaches

Management accounting tools can be classified according to various criteria, depending on methodological approaches.

1. Depending on the volume of information processed, the formation of management accounting can be:

- Systematized.

Conducted on a regular basis, it includes measurement, assessment and control of costs for all types of processes (supply, production, sales). All costs are grouped by items and elements, sources and media. An internal report is being compiled, the content, timing and frequency of provision of which satisfy internal users and allow an assessment of the activities of the enterprise as a whole and individual structural divisions. - Differentiated.

The content is selective and depends on the objectives.

2. Depending on the goals and objectives of management, the formation of management accounting can be:

- Strategic.

Focuses on determining the company's development prospects and providing information to senior management. - Operational.

Ensures achievement of goals in the short term - Production.

The task is to provide information about the cost of production, the amount of profit, and the cost of inventory.

3.Depending on methodological approaches to organizing management accounting, the following can be used:

- Integrated (monistic) system. The management system is interconnected with the financial system. The chart of accounts in the management system is linked to financial accounts.

- Autonomous (dualistic) system It is assumed that management and financial systems will be created separately. The chart of accounts of the management system is not linked to the financial one. The process focuses only on management needs.

4. In terms of the scope of activities and organizational structure of enterprises, the management system can be:

- Complete system. This type applies to the activities of the enterprise as a whole and its individual structural divisions.

- A sufficient system (with a limited set of indicators). The essence of this type is that it is carried out only for individual objects or their group.

5. For efficiency and data control, accounting can be used:

- Factual data.

The method of attributing actually consumed resources to expenses, calculating the actual cost and financial results from product sales is used. - Regulatory data.

In this case, it is assumed that certain cost norms will be developed and accounting will also be carried out according to norms (standards) with deviations highlighted.

6. Based on the completeness of costs, the following types can be distinguished:

- Full costs.

The cost price is calculated by including all costs - Marginal.

The reduced cost is calculated.

Rules promoting the effective implementation of management accounting in an enterprise

Automation of management accounting should be a systematic process. In practice, when solving this problem, company managers, even in Moscow, the center of concentration of business information, make a number of typical mistakes, the correction of which leads to additional financial costs and loss of time. To avoid such problems, keep the following rules in mind.

1. Internal management reports should contain only the necessary information and be in a form that is easy to understand. They should be structured, easy to read, and visual. They should include only those details that are necessary for management purposes. This approach not only reduces document processing time, but also makes them more informative and useful.

2. The assessment of reporting elements should be made not only on the basis of financial methods, but also using other methodologies. When creating rules, international standards should be used along with Russian rules.

3. Effective implementation of automation of management accounting can be carried out only after a detailed diagnosis of the company and carrying out explanatory work among managers about the need for such an action.

4. A significant number of employees should be involved in the process of creating management accounting, since a fairly wide range of personnel will use the information base for the purpose of managing and implementing the sales process. This task cannot be entrusted only to accountants, economists and financiers.

5. When implementing automation of management accounting, it is necessary to accurately determine the scheme of business processes, optimize it and distribute functions, create job descriptions. This approach will avoid duplication of functions.

6. The introduction of management accounting involves solving a whole range of problems in order to increase the efficiency and quality of management and improve performance results in all areas. Therefore, it cannot be focused on solving a single problem. For example, ensuring document flow.

7. The process of improving the formation of management accounting should be permanent. It is impossible to allow optimization carried out once to be considered a sufficient action. The system must be regularly improved, new software products introduced and innovative methodologies used.

8. It is necessary to create document flow regulations that specify the deadlines for submitting documents, submitting reports, and motivating staff for compliance with the rules. A document flow schedule can be an effective solution.

9. Corporate culture involves the exchange of information within precisely defined time frames. The introduction of information technology makes it possible to effectively implement this process.

10. Management accounting tools must correspond to the tasks set by the company. Limitation of capabilities due to technical factors should not cause additional problems at the enterprise.

Management accounting in “WA: Financier” (1C 8 platform) - a modern solution

As a company develops, its organizational structure becomes more complex, and the volume of information processed increases. There is a need to automate processes. Effective organization of a management system is inevitably associated with the use of various software products. A significant number of business transactions, a large range of goods, a large list of counterparties - this is a small part of the list of criteria that contribute to the complexity of the process.

In the first stages after the creation of an enterprise in Moscow or another city in Russia, management accounting can be carried out using simple EXEL tables. This approach is effective for small volumes of business transactions. It is quite natural that with a small amount of start-up capital, small enterprises resort to methods that can be obtained for free. As a company grows, not only the number of business transactions that can be processed increases, but also the amount of capital that can be invested in information technology and software. Special programs provide systematization and efficiency of obtaining information. The most popular solution to the problem is the implementation of management accounting tools in “WA: Financier”.

Large companies use ERP systems that allow them to maintain all types of accounting simultaneously. But such solutions are very expensive.

Conducting forecasting at an enterprise using automated management accounting allows you to quickly process significant amounts of information. In combination with additional modules, the system's functions can be expanded. Users receive a number of benefits:

- a wide range of tools for accounting and control, allowing you to quickly obtain information and analyze it from various angles;

- the systems and modules used are easily customizable in accordance with the accounting policy and specifics of the company’s activities;

- High performance of automation tools allows you to instantly process significant amounts of information.

Automation of management accounting

Management accounting programs allow you to solve problems of process automation, control and reporting. Universal and effective solutions are the “WA: Financier” line of software products. They can be used at enterprises with different specifics and volumes of document flow at enterprises in Moscow and other regions of Russia. They are effective for use in organizations with a dedicated financial service, as well as in companies that operate with aggregated data received from external systems.

Suggested modules for automation:

- To ensure the efficient operation of the treasury and the formation of the cash flow management system, the “Cash Management” module (abbreviated as “UDS”) can be used;

- To create a budget of income and expenses and a forecast balance sheet, the “Budgeting” module is used;

- To maintain management accounting according to corporate standards and IFRS, the “Management Accounting/IFRS” module can be used;

Using “WA: Financier” software products, you can implement various options to ensure automation of accounting and budgeting processes.

A. Budgeting.

To solve budgeting problems and automate processes, you can use various “WA: Financier” products:

1. If it is necessary to implement a full range of budgeting, use the module “WA: Financier. Budgeting."

2. If the enterprise is tasked only with cash management on the basis of cash flow records, the “WA: Financier” module can be used. UDS".

B. Operational management accounting.

To effectively organize operational management accounting and automate the process using WA: Financier products, you can use the following solutions:

3. For operational accounting of cash flows, the module “WA: Financier” is used. UDS" (Cash Management);

4. For management accounting, it is effective to use the module “WA: Financier. UprUchet/IFRS";

5. If for operational accounting and analysis of working capital it is necessary to use the functions of reserving goods, complex cost calculations and other specific trade operations, then the module “WA: Financier. UprUchet/IFRS" is used as an addition to a specialized program for management accounting (for example, in 1C 8 Trade Management). In this case, the system will provide automation of the purchasing and selling functions, and the module “WA: Financier. UprUchet/IFRS" - functions of the financial service for transmitting operational analysis data.

B. Management reporting.

The following modules can be used to generate and analyze reports:

6. By cash flow - “WA: Financier. Cash management";

7. "WA: Financier." Management Accounting/IFRS" - for the generation of management (internal) reporting and financial (external) reporting, including according to IFRS standards.

Send this article to my email

Management accounting in 1C is presented in the form of a series of analytical reports, on the basis of which it is convenient to analyze the organization’s activities, identify problems and make management decisions. All reports in the program are located in a separate section called “Manager”. They contain all aggregated information on primary data. Also, most reports are generated in the form of charts and graphs, which is very convenient for perception.

As you can see, for ease of use of these reports, they are divided into appropriate groups. In this article, we will consider several reports for management accounting in 1C. Let’s generate the “Income and Expenses” report by selecting the period and organization.

Please leave the topics that interest you in the comments, so that our experts will analyze them in instructional articles and video instructions.

The report will display a chart and table with the values of income, expenses and profit. If necessary, we can decipher each period and see the documents. In order to see the structure of the company’s assets, we will generate a report “Current assets”.

The chart and data show that assets are growing. However, in the structure of assets there is an increase in buyer debt in the last months of the selected period. Efforts must be made to ensure that this asset becomes more liquid, i.e. into cash.

Let’s generate a report from the “Sales” group, for example “Sales by counterparties”.

The diagram immediately shows which counterparties our organization sold the most goods to. For more detailed information please refer to the table. It is also possible to customize the report using the “Show settings” button in the header.

In this case, an additional “Nomenclature” grouping has been added to the report; also on the “Selection” tab, you can set selection, for example, by the counterparty or item item of interest to us. Then you need to reformat the report.

If necessary, you can make a selection by warehouse or product item in a similar way. Next, we will create an interesting report “Customers’ debt by debt terms” from the “Settlements with customers” group.

Once formed, you can see overdue debt and group overdue debt by how long the debt has been overdue. We can adjust the delay intervals by adding the ones we need or removing those that are not interesting to us. You can also do this by clicking the “Show settings” button. Similar functionality of reports in the “Accounts payable” group.

And for example, let’s generate another “Financial Analysis” report from the “Analysis” section. The report has several tabs. The “Main” tab displays information about sales and net profit. Also liquidity ratios, company profitability indicators, assessment of bankruptcy risk and creditworthiness.

The “Accounting Statements” tab presents the balance sheet and financial results statement. If necessary, enterprise managers can configure rights so that they have access only to the section discussed in this article.

The 1C company traditionally pays great attention to the development of management accounting functions in its products. Today, on the market of systems built on the basis of the 1C 8.3 platform, three categories of software products can be distinguished that allow management accounting in 1C:

- 1C company products that solve the problems of complex automation of enterprise activities, including such functions as automation of management accounting.

- 1C company products that solve the problem of consolidating data from other systems (including first category systems) and obtaining management reporting.

- Programs of third-party companies (1C Franchisees) that solve specialized problems of management accounting.

The basis of management accounting and its essence is management reporting, used by managers at different levels to control the activities of the enterprise, planning and making decisions based on the data supplied by this reporting. Therefore, despite the variety of systems and the often existing differences in approaches to processing and presenting data, the functionality of the systems is similar, and the main differences lie in the architecture, positioning and method of implementing functions.

Solving problems of automation of management accounting in 1C based on complex information systems of the company 1C

It is best to consider the functionality of solving complex accounting automation problems based on 1C using the example of the company’s flagship solution “1C: ERP Enterprise Management”. Other configurations, to one degree or another, also make it possible to solve the problem of obtaining management reporting, but 1C ERP contains the most complete set of capabilities and approaches to obtaining management reporting.

Accounting in 1C ERP can be divided into several logical reporting blocks:

- Operational reporting used at all levels of enterprise management;

- Regulated reporting, used primarily for transmission to fiscal authorities and external users;

- Budget reporting for the purposes of planning the financial activities of an enterprise and monitoring the implementation of plans;

- International financial reporting (IFR), typically used to provide information to external users.

From the presented list, only operational reporting is mandatory in 1C ERP. We can say that it is an inseparable part of the system, and it cannot be disabled by the settings of the application solution. The remaining functional blocks are switchable; if necessary, you can refuse to use one or more accounting sections, which will generally simplify the interface and speed up the operation of the system.

In addition to the tasks of obtaining reports, 1C ERP solves related problems related to data protection and reporting:

- Separation of access rights, both for specific reports and in general for data available for analysis;

- Visualization of data in any form (both customizing the appearance of reports and using widgets for quick access to key performance indicators of the company);

- The ability to remotely connect to the system and gain access to reporting, including using mobile devices.

Operational reporting in 1C

The system contains more than a hundred reports intended for both line personnel and enterprise managers. And taking into account the fact that each report is customizable, a kind of mini-constructor, there is an almost unlimited number of options for the final reports of the operational circuit.

Figure No. 1. Sales reports

Regulated reporting in EPR

Data in the regulated circuit is consolidated within the system according to the operational circuit data and reflected in the RAS chart of accounts. To analyze the received reports, standard accounting reports are used: SALT, account card, etc.

The specificity of the regulated reporting block is that it is the least customizable of all, since the reporting requirements are dictated by the requirements of current tax legislation and PBU, that is, they can greatly diverge from the management accounting policies adopted by the company.

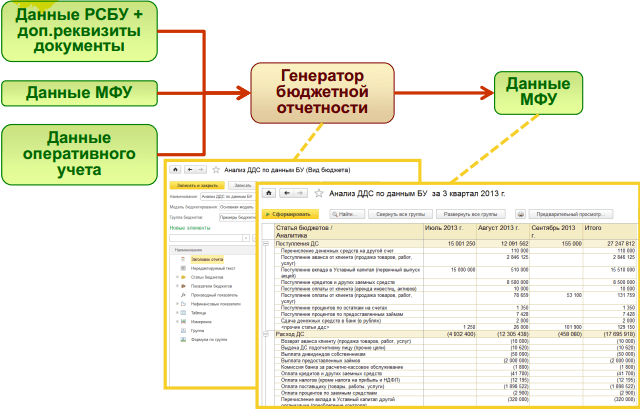

Budget reporting and MFIs

Unlike operational and regulated reporting, where the 1C system already contains pre-configured reports, management reporting of budgeting blocks and multifunctional financial functions requires preliminary development. This is due to the fact that the requirements for such reporting, the rules and procedure for obtaining can vary greatly in different companies, which means that such reporting needs to be developed to suit the needs of a specific organization.

Figure No. 2. The principle of generating management reporting for management accounting purposes

Figure No. 2. The principle of generating management reporting for management accounting purposes

Visual design of key indicators of management activities

It is worthwhile to dwell specifically on the mechanism for visually presenting key indicators of an enterprise’s performance. 1C ERP contains mechanisms for visual presentation of data that allow you to quickly assess the status of key indicators of an enterprise’s performance.

Figure No. 3. Presentation of key indicators in 1C ERP

Figure No. 3. Presentation of key indicators in 1C ERP

Widgets are fully customizable; as you work, it makes sense to visually display the indicators that are of key importance to your company.

Obtaining consolidated management reporting based on 1C products

The 1C company has only one solution specifically designed for the purpose of automating data consolidation and obtaining management reporting - 1C: Holding Management (HW). The product consists of a set of subsystems that implement several different management layers:

- A layer of subsystems for improving corporate performance, including:

- Obtaining consolidated management reporting and IFRS reporting;

- Budgeting for operations and projects;

- Business analysis and balanced scorecard.

- The layer of subsystems that are usually associated with corporate controlling:

- Centralized procurement management;

- Centralized treasury;

- Contract management

- The layer of corporate accounting systems is represented by:

- Corporate tax management system;

- Accounting system.

Since the solution is primarily intended for automating management accounting of management companies and financial services of business units of geographically distributed IT landscapes, the center of the system is the integration functionality, i.e. the solution is usually used either as a corporate template or as a solution for management companies (holdings).

Figure No. 4. Schematic functional diagram of 1C Holding Management

Figure No. 4. Schematic functional diagram of 1C Holding Management

It should be remembered that the solution is intended primarily for large organizations, including those with the status of a large taxpayer, therefore the functionality of the system is primarily intended to solve the problems facing such enterprises:

- Consolidation of data from external systems, including the ability to directly connect to a DBMS, and obtain information from arbitrary Excel files;

- Preparation of financial statements according to IFRS standards;

- Implementation of budgeting and treasury functions taking into account the needs of large enterprises (building complex budget models, multi-level management of budget processes);

- Setting up and visualizing the Balanced Scorecard (BSC);

- Management of investment programs and analysis of investment projects;

- Preparation of reports of controlled foreign companies;

- Corporate tax management.

Programs for automating management accounting of third-party companies (1C franchisees) on the 1C 8.3 platform

On the market, in addition to the direct products of the 1C company, there are a large number of programs built on the 1C: Enterprise 8.3 platform that solve the problems of automating the functions of management accounting and the financial block as a whole. These solutions are developed and supported by 1C partner companies (franchisees) and must necessarily have a “1C-Compatible” certificate.

Despite the variety of solutions and declared functionality, the architecture of the products is built on a similar principle and resembles the 1C UX solution (adjusted for the scale of the tasks being solved): consolidation of data from external systems and further conversion of data for the purpose of obtaining the necessary reporting. The leaders in the market for such systems are Wiseadvice Financier, Bit-Finance, Intalev “Corporate Management” and a number of others.

Results

If we talk about which management accounting program makes sense to choose for implementation, then there is no universal answer to this question; in each specific case, a choice must be made based on the needs and capabilities of a particular organization. However, successful automation of management accounting may have some general recommendations:

- If a company is faced with the task of implementing a system of comprehensive automation of activities, and solving the problem of implementation in a future management accounting system is considered as part of the implementation task, first of all it is worth considering complex 1C configurations, for example, 1C ERP Enterprise Management.

- If a company has already implemented an activity automation system, but needs to solve specific problems of obtaining management reporting, it makes sense to think in the direction of specialized solutions: for small and medium-sized companies, solutions from 1C partner companies built on the 1C 8.3 platform are best suited. For large companies, it makes sense to look towards the 1C: Holding Management product.

We briefly reviewed the classes of systems for automation of management accounting currently available on the Russian market.

The choice of an information system for automating a company’s management accounting depends on its needs. Large enterprises that need complete and detailed information implement expensive ERP systems, while small companies often use Excel for these purposes. At the same time, many companies maintain management accounting using accounting systems. We decided to talk in more detail about this method of organizing management accounting by interviewing users of the most widespread accounting program in Russia, “1C: Accounting,” as well as specialists from companies involved in its implementation.

Magazine "Financial Director" No. 3 (March) 2004

Collection of information

There are three main options for collecting and processing information in the 1C program, which are typical for working in any accounting systems.

First option. Management and accounting data are collected and entered into the appropriate databases separately. There are no problems with comparing information bases, since this is not necessary. However, this option is very labor-intensive.

Second option. Management accounting data is obtained by converting accounting data. But fully automated data transfer is hardly possible, since accounting information needs to be supplemented. For example, the shipment of a computer assembled by a company can be reflected in accounting as a shipment of components, and their assembly into a complete model can be reflected as a separate service. At the same time, in management accounting, the shipment of a computer can be reflected as a series of operations (moving components for assembly, assembly, shipment of a unit of production). Therefore, it is easier to reflect such transactions separately in accounting and management accounting.

Third option. Accounting data is obtained from management accounting data. At the same time, operations related to core activities (purchases, sales, production) are most often uploaded from the management database to the accounting database. There is also parallel separate accounting of operations that differ in content in accounting and management accounting. This method is the most technologically advanced. However, since management accounting data is entered into the database, as a rule, by direct executors or economists, and then automatically transferred to the accounting database, the accounting department may lose control over the accounting process. To prevent this from happening, the most typical operations are usually automated, and the rest are recorded by the accounting department.

Our research has shown that users of 1C accounting modules most often use the first option. This is, in particular, due to the fact that accountants of medium and small companies, as a rule, do not want to take on the additional burden and responsibility of maintaining management accounting and at the same time oppose interference in their area of activity by other employees. In such companies, management accounting is handled directly by the financial director (sometimes the head of the enterprise) or by a department independent of accounting, for example economic planning. In addition, management accounting and budgeting are often not defined as management technologies and one or two people are responsible for making decisions, who are consumers of financial information, and the information itself is clearly divided into “black” and “white”. In such companies there is no need for complex automation systems, so a parallel database in the 1C: Accounting program is used to maintain management accounting.

As business grows and management skills improve, companies abandon the simplified approach, preferring to fully automate data transformation, that is, they move to the second or third options. This usually increases business transparency.

In the second and third options, the working chart of accounts, on the basis of which management accounting is maintained, is constructed similarly to the chart of accounts for financial accounting, using additional analytical features or subaccounts for accounting for transactions in management accounting 1 . In such a situation, you can enter the bulk of the data once, and then create the required management and accounting reports by sampling according to analytical criteria or subaccounts.

- Personal experienceVadim Lebedevich

Our management accounting methodology in some places differs significantly from the accounting methodology. If you conduct management accounting directly in the circulation version of “1C: Accounting” in parallel with accounting and tax accounting, then the program will have to be reconfigured too often after updates related to changes in legislation. Therefore, it has become more effective for us to maintain management accounting in a specialized system developed on the basis of 1C: Enterprise.

Evgeniy Fadeev

In order to achieve one-time data entry, it is necessary to establish rules by which information from accounting can be transferred to management. Then these rules simply need to be described in the program.

Data must be processed repeatedly if such rules are not developed, or employees who process information for one of the accounting sections, for example accounting, cannot determine how this information should be interpreted for management accounting purposes. In this case, the economic department is responsible for transferring accounting data to the management accounting database.

Tatiana Borisovets

We keep all records at the place where the operation occurs, that is, the postings are entered into the system by employees of the sales departments, warehouse and production shops, and all the necessary analytical characteristics are entered. Later, the accounting department checks the system data with the primary documents.

Let's look at the differences between the three ways to obtain management information using an example.

- An example of accounting for a business transaction in 1C: AccountingOperation description

Registration of a fixed asset (computer) and registration of an account statement.

First option

Registration. The computer is taken into account in the accounting database, a fixed asset card is filled out, which indicates the service life, date of registration, purchase price, etc. Then the fields of the card, which will be the same for both types of accounting (inventory number, name, financially responsible person, place of operation, type of fixed asset) are copied to a parallel database. The remaining fields required for management accounting (depreciation period, cost of fixed assets, cost item, etc.) are filled in manually.

When accounting for a fixed asset, the relevant documents reflect a standard set of operations: commissioning, transfer of a fixed asset, movement, receipt, write-off. Based on these documents, accounting entries are automatically generated in 1C: Accounting. Other transactions may be reflected in management accounting, so entries are made manually.

Account statement. The extract is registered in accounting according to standard rules and copied (automatically or manually) into the management accounting database.

Second option

Registration. Fundamentally no different from the first option.

Account statement. Information about the status of accounts is received by the accounting department, as a rule, promptly. Data can be simply imported into the management database. If accounting information is too detailed, the detailed entry is “collapsed”. For example, for accounting it is important to divide into “payment” (account 62.1) and “advances” (account 62.2). In management accounting, such a division is not important in some cases, so such transactions can be automatically combined.

Third option

Registration. When transferring data from management accounting to accounting, you will have to fill in the fields of the fixed asset card required for accounting. In addition, since accounting for fixed assets in management accounting is carried out in the form of double entry, information about them will also have to be imported into the accounting database in the form of transactions. You will also have to account for fixed assets in the accounting database using postings, and this is labor-intensive. Therefore, if there is a large number of fixed assets, it makes sense to modify the program so that it is possible to automatically transform management accounting entries into accounting documents.

Account statement. Let's say the client paid an advance for shipped goods and the accountant entered the following entry into the management database: Debit 51 Credit 62. For the purposes of management accounting, it does not matter whether there is an advance or payment. For accounting purposes, on the contrary, a clear division into advance and payment is necessary. Therefore, it will not be possible to automatically transform a posting from management accounting to accounting. To solve this problem, it is necessary to provide the ability to enter the payment type in an electronic document in management accounting.

The example was prepared by Vadim Lebedevich

In addition to the different interpretation of operations in accounting and management accounting, there are also problems of combining these types of accounting 2. In mass-produced versions of accounting programs, including 1C: Accounting, it is very difficult to organize the accounting of non-financial indicators (for example, the number of seats per square meter of area, the percentage of defects per employee). Therefore, when maintaining management accounting, there is a need to supplement and adjust data from accounting systems.

Despite the fact that in the corresponding modules of “1C: Enterprise” (for example, “Financial Planning”) it is possible to take into account non-financial indicators, all study participants emphasized that the Excel program is usually used for this purpose. Thus, in the “Ideal Cup” company, when calculating the cost of products, its components, which differ from those reflected in accounting, are manually transferred from Excel files to the “Financial Planning” module. According to Marina Sheludko, it would be more convenient to keep records in a single circuit. Currently, company employees have to use settings to download part of the data from 1C: Enterprise. Complex configuration" in "1C: Financial Planning", and enter some of the data manually.

Another problem when automating management accounting using 1C: Accounting is accounting for settlements between responsibility centers within one legal entity. In accounting, such transactions, as a rule, are not reflected at all, but in management they must be reflected. This problem can be resolved using additional settings.

- Personal experienceStanislav Sharipov

- an account is entered that records transactions that can affect settlements between departments (or a register for the “Operational Accounting” component);

- new documents are created that reflect various transactions that affect mutual settlements between departments;

- Special reports are being developed to provide information on payments between departments.

Our clients rarely need to automate payments between internal departments. However, if you need to account for internal settlements, then it can be configured similarly to the scheme for accounting for mutual settlements between the organization and external counterparties. To do this, you usually perform the following steps:

Budgets for companies that use “1C: Enterprise” are compiled either in Excel or in the appropriate applications (“1C: Financial Planning”). If a 1C-compatible program is used as a budgeting system, automatic loading of actual accounting data is possible, so you can monitor the implementation of the plan regularly (even daily).

Conducting an operational analysis of deviations of actual indicators from planned ones is possible provided that most of the data is entered into the system on the basis of transactions, information about which is entered by local performers, and not based on primary documents received by the accounting department. At the same time, at the time of entry of the transaction information about it may not be documented. For example, in the Kalandr company, where this approach is implemented, the results of the previous day according to the state of the company’s cash flows are included in the 1C: Financial Planning module every day before 11 am.

- Personal experienceMarina Sheludko

In our company, planning is carried out in the 1C: Financial Planning module. Planned indicators are entered by managers and employees of the relevant departments. Actual data on the execution of the cash flow plan (from payment orders, memos, etc.) first enters the “Financial Planning” module and is then transferred to the accounting department for processing. This allows you to monitor your progress on a daily basis. The accounting department receives only confirmed documents, which end up in the 1C: Enterprise module. Complex configuration." Cash control is carried out daily, and we prepare full reports on a monthly basis. Part of the data for full reporting is first processed in the “Complex Configuration” block and then goes to the “Financial Planning” block (production, losses, etc.).

Analysis of the collected data occurs using either the tools of one of the specialized modules “1C: Enterprise” (“Financial Planning”), or Excel. At the same time, all study participants use both standard reports (income statement, balance sheet and cash flow statement) and additional reporting forms.

- Personal experienceTatiana Borisovets

In order for management accounting data to be available to all middle managers, we had to add reporting forms reflecting the activities of different departments. Thus, the technical department was able to analyze the consumption of raw materials. Reports have been added: “Shipment of finished products by type” (for the marketing department), “Turnover of goods in warehouses” (sales department), “Accounting for the movement of material resources”, “Production costs by type of product”, etc. We are now working on maintaining custom accounting for certain types of production. In addition, we set up the system so that we can organize prompt (daily) write-off of raw materials. As a result, all analysis of management information is carried out in 1C: Enterprise.

Marina Sheludko

Using the “Financial Planning” module allows you to view standard reports in various sections (divisions, items, indicators) and, if necessary, drill down into these reports to identify the reasons for deviations from the plan. Thus, we will find out which indicators affect the value of a particular budget item. In addition to the three main ones, we also use other reports, but they are generated mainly in Excel, since the “Financial Planning” module is a static tool.

Technical aspects

Certain problems when using accounting systems, in particular 1C: Accounting, are associated with the fact that users tend to use a cheaper (and therefore low-power) version of the program and inexpensive equipment. Therefore, difficulties arise when processing large amounts of data. However, these problems can be avoided.

According to Tatyana Borisovets, at their enterprise (about 700 people), even when generating a monthly cash flow report, uploading data to the report takes only a few minutes. Stanislav Sharipov believes that it is difficult to accurately estimate the number of transactions that can overload the system: “Suppose a company of 300 to 900 people buys a package of 1C modules and equipment for current needs and at the same time continues to develop dynamically. If the number of operations per month reflected in the system reaches 5000-7000 or more, then the company will have to spend money on a more powerful version of the program and more productive equipment after 1-2 years of operation in this mode.”

Another method that is used to “unload” the system is to copy information about past accounting periods onto backup media (CDs, additional servers, etc.). This will help reduce the amount of analyzed data, which, if necessary, can be accessed as an archive.

As for restricting access to system data, the users we interviewed use standard means: prohibiting viewing by data groups and editing closed periods, etc. You can also use additional levels of protection, for example, electronic keys, database encryption, etc. in most cases the costs are minimal.

Results of the study

The study showed that the organization of management accounting based on the 1C: Accounting program is suitable for companies that have low requirements for managing and analyzing data about their activities. These include small and medium-sized enterprises or branches of large corporations, in which management functions are carried out mainly from the “center”. This system is more in the interests of accountants than of managers, including financial directors. Therefore, to obtain information about the company’s activities, additional 1C: Enterprise modules are needed and may require modification to take into account the requirements of managers.

Although maintaining management accounting in 1C is the simplest and most economical way to organize management accounting both from a financial point of view and in terms of labor costs, it will still require additional resources from the enterprise.

- Tatiana Borisovets After automation of management accounting, the number of functions for ordinary employees increased. If previously a warehouse worker only accepted or released goods, now he accepts money, checks the customer card and payment history. The sales department began selling services and issuing certificates of their provision. It was possible to streamline document flow at the enterprise. We purposefully made 1C a unified accounting system for all departments.

It should be noted that all the above conclusions do not apply to the 1C: Enterprise 8.0 system, which, according to the developers, should significantly expand the capabilities of company management. As soon as practical experience in using this system appears, we will definitely talk about it on the pages of our magazine.

The material was prepared by magazine expert Anna Netesova